If you are saving for a child’s college, you are probably already aware of Iowa 529 accounts. These accounts provide tax free growth of your investments and give you a state tax deductions for contributions.

While many people we talk to know the basics about these accounts, we also find a few aspects of these accounts that most are unfamiliar with:

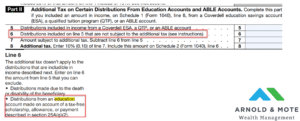

What if Your Child Gets a Scholarship?

First, if your child receives a scholarship, you have the ability to take money out of your 529 penalty free equal to the amount of the scholarship.

Below is where you indicate on your taxes that a withdrawal is due to a scholarship and therefore not subject to additional taxes or penalties.

Many parents worry that they may save into these 529 accounts and end up not needing the money. Thankfully, there are many provisions in the rules for Iowa’s 529 plan that limit the penalties and taxes you would be subject to from leftover money in a 529 account.

Use Savings Bonds for Added Tax Deductions

Next, savings bonds can be rolled into 529 accounts interest free and also provide you a tax deduction.

Many people are familiar with US Savings bonds (Either EE or I series). However, when you sell or redeem these bonds, you are taxed on the interest that they have earned.

Contributing to a 529 is a qualified education expense for savings bonds, meaning that cashing them in and using the proceeds to fund a 529 account can be done completely tax free. This saves you from paying taxes on the interest of the savings bonds AND you also get the state tax deduction for making a contribution.

One caveat though, check that your income is within the range that allows savings bonds to be used tax free for qualified education expenses. If you are above a certain amount of income this may not work for you.

Rollover Out of State 529 Plans

Lastly, you can roll other state 529 accounts into an Iowa 529 and get an Iowa state income tax deduction.

This is a valuable if you have previously been sold an out of state 529 by another financial advisor, or if you open 529 accounts in other states to take advantage of matching contributions or special incentives offered for new accounts.

The state’s maximum annual deduction for 529s still applies for transfers though. So if you are moving a large account it may be worth splitting into several years to take full advantage of the tax breaks.

Also note, if you took a tax deduction from your contributions to the out of state plan (for example, if you used to live in that state), states may have clawback provisions that require you to pay back the tax deduction you took at the time of contribution.

Learn More About Iowa’s 529 Plan

If you are interested in learning more, here’s a more detailed webinar we did on Iowa’s 529 Plan.

Matt Hylland is a financial planner and partner at Arnold & Mote Wealth Management, where he helps individuals and families make informed decisions around retirement planning, investment management, tax planning, and comprehensive financial strategy. As a flat-fee, fiduciary advisor, Matt focuses on providing objective guidance designed around each client’s goals and long-term financial needs.

Before transitioning into financial planning, Matt worked as a materials scientist for the Department of Defense, bringing a problem-solving mindset and analytical approach to his work with clients. He has been featured or quoted in nationally recognized financial publications, including The Wall Street Journal, CNBC, and Kiplinger, for his insights on personal finance and investing.

Years of experience: 10

Specializations: retirement decisions, tax-efficient strategies, investment choices, and the complex financial decisions that come with major life transitions.