Qualified charitable distributions, or QCDs, are almost always the most tax efficient ways to give to charity. However, they are only available for those of a specific age, and with a specific investment account. Here we cover what you need to know to be eligible to perform QCDs, and the rules in order to receive the tax benefits.

What is a Qualified Charitable Distribution (QCD)?

A QCD is a distribution made directly to a charity from an IRA. This allows you to donate directly from your retirement accounts, and avoid taxes that would normally result from IRA withdrawals and Required Minimum Distributions (RMDs). For most, they are the primary tool of a retiree’s charitable giving plan.

QCD Rules:

1) You must be at least 70.5 years old.

Not 70, but 70 and a half years old! You can only begin to donate via QCDs once you have turned 70.5 years old.

2) You have a traditional IRA.

It must be an IRA, you can’t do this from a 401(k).

You can donate via a QCD from an inherited IRA account if you are over age 70.5.

3) Maximum of $100,000 per year.

You are only allowed to donate $100,000 per year through QCDs (Calendar year 2023). Beginning in 2024, that amount will be adjusted for inflation.

Tax Advantages Of QCDs

Why are QCDs almost always the best way to give to charity?

If you take a distribution from your IRA and send the proceeds first to your bank account and then give to charity, you’ll be taxed. Worse yet, that IRA withdrawal could impact your Medicare IRMAA surcharge and cause you to pay more for Medicare.

With QCDs, the money goes straight to the charity, never to your bank account and therefore is not subject to any taxes.

You do not get a tax deduction from doing QCDs. Instead, it is never even taxed at all!

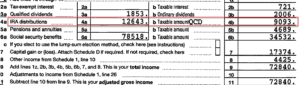

Here’s how it will look on your tax return:

Notice that the household in the above return withdrew $12,643 from their traditional IRA during the year. However, not all of that $12,643 will be taxable to them because they donated $3,550 via qualified charitable distributions. That leaves only $9,093 of their IRA distributions resulting in taxable income.

Offset Your RMD

You can begin doing QCDs at age 70.5, but an even bigger advantage comes a few years later, when your RMDs (required minimum distributions) begin. If you do not need your RMDs to help fund general living expenses, RMDs typically result in unnecessary additional taxes.

However, QCDs will reduce your RMD, helping you avoid this unnecessary tax liability.

For example, if your required minimum distribution is $10,000 and you donate $7,000 via QCDs during the year, you will only need to withdraw $3,000 from your retirement accounts to satisfy your annual RMD.

How Do Qualified Charitable Distributions Work?

How do you do a QCD? For clients of Arnold and Mote Wealth Management, you receive a special checkbook only for charitable giving. This checkbook makes donating, and record keeping for tax purposes, easy. It is as easy as writing a check!

Get Help With Your Charitable Giving Plan

QCDs take coordination with your overall retirement plan, your financial advisor, and your tax preparer. If you have questions about how to use QCDs to maximize your impact to charities, and save yourself some tax liability, please reach out.

Matt Hylland is a financial planner and partner at Arnold & Mote Wealth Management, where he helps individuals and families make informed decisions around retirement planning, investment management, tax planning, and comprehensive financial strategy. As a flat-fee, fiduciary advisor, Matt focuses on providing objective guidance designed around each client’s goals and long-term financial needs.

Before transitioning into financial planning, Matt worked as a materials scientist for the Department of Defense, bringing a problem-solving mindset and analytical approach to his work with clients. He has been featured or quoted in nationally recognized financial publications, including The Wall Street Journal, CNBC, and Kiplinger, for his insights on personal finance and investing.

Years of experience: 10

Specializations: retirement decisions, tax-efficient strategies, investment choices, and the complex financial decisions that come with major life transitions.