Life insurance is an important part of any financial plan. But, just because a specific insurance policy was right for you in the past does not mean it still belongs in your plan!

You should perform a review of your life insurance and long term care insurance annually, or when you have significant changes to your financial plan. This helps ensure that you are not wasting money on unnecessary or overly expensive life insurance policies.

In this webinar we look at how to analyze your current policies, including:

- Term Life Insurance,

- Annual Renewable Term Life (Term 80+ for example)

- Permanent Life Insurance

- Whole Life Insurance

- Universal Life Insurance

- Long Term Care Insurance (LTCi) and Hybrid Long Term Care Insurance

How to Do An Annual Insurance Review

Why Review Insurance Regularly?

To start, why is reviewing insurance policies regularly important to do?

First, a majority of Americans have some sort of life insurance. So this is a topic that impacts a lot of people.

It also can be a pretty significant expense. Especially if you are looking at permanent life insurance, like whole life or universal life, and long-term care insurance. If you are paying for insurance you don’t need, that’s a lot of money going towards something that might not have a great return.

And its also something that tends to be put in place at one point in time and rarely looked at again. Maybe you buy that whole life insurance policy when you are 35 years old, and just keep paying the premiums and never look at it again until for another couple decades.

This leaves room for opportunities to review because in general, your need for insurance will decline over time.

When you are 30 years old, you have a lot of future expenses to cover, and a lot of potential loss of income. For most, this is when your largest insurance need will be.

Then, as you age you have less and less future loss of income to protect against, and your savings give you or your spouse a source of funds as well to use in case you pass away early.

This concept works for life insurance and also long term care insurance as well.

Maybe you bought that long term care insurance policy when you were 60, when the prospect of a large long term care expense early on would put your plan at risk. But now you are 75, your investments have performed well, you are still on track with your plan, and you are in much better position to be able to self-insure than you were 15 years ago.

So regardless of whether we’re talking about life or long term care, if you haven’t looked at your policies for years or decades, there’s likely room to adjust coverages.

Another Reason to Review Insurance Regularly

And then of course, besides just the general reduction in insurance need over time, your plan can change over time as well.

When you purchased that term insurance policy 15 years ago, maybe you had much lower income, but you have since received a promotion and increased your savings. Now that insurance amount that was adequate 15 years ago, is unnecessary today.

I think you get the point, there’s lots of things that can change with your plan over time, and if you have had a significant change here in any of these items, there is a significant change in your insurance need as well.

What to Review on Your Term Insurance

Starting with the most simple insurance – just basic term insurance.

This insurance just provides a set benefit amount for a certain number of years for a certain premium, which is sometimes fixed and other times not.

So there’s not a lot of different variables to analyze here, the 2 main ones are;

First, the years left on the policy.

Is that term still appropriate? If you have increased savings you might not need insurance for as long as you initially thought. The option is available to you to surrender this policy and save the premiums.

Or, do you now need insurance for a longer term? Maybe you had another child, or took on debt later in life that led to a larger insurance need. The earlier you identify an increased need for insurance, the better because insurance premium rates only increase over time. So address any shortfall now, rather than later down the road.

So, no complicated calculations here, nothing groundbreaking. But, also something that most people just don’t think about and consider over time.

Don’t Forget About Employer Life Insurance

And one other variable we like to make sure you are thinking about is the basic life insurance benefit provided by an employer, if this applies to you of course.

A lot of times companies provide 1 or 2 times salary for no out of pocket cost for employees. This might leave you with a good amount of insurance to have later on in life, and give you the confidence to be able to cancel other outside policies. It can be a good way to step down your insurance amount, you aren’t leaving yourself with nothing, but can save some money by reducing benefits slightly.

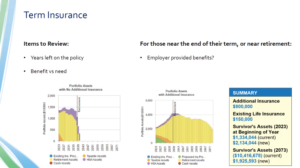

How We Analyze Term Insurance

And this is easy for us to help you with. We can perform what is called a Gap Analysis to look at what would happen to your plan if you or your spouse would pass away early (or become disabled, or need long term care), and then calculate the insurance that is needed to fill that gap and make your plan successful.

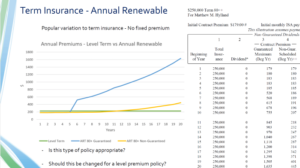

Annual Renewable Term (Term 60+, Term 80+, etc)

There is one last item we wanted to mention about term insurance, and that is what is called annual renewable term life.

From my experience these are marketed pretty heavily by the big insurance companies, the one we are looking at here is a quote I received from Northwestern Mutual. But you’ll see something very similar from a lot of different companies out there.

The big difference here is that the premiums are not fixed, or level, like most of the term policies we look at with you. The premiums start low, but will increase over time.

Just for this example, what we are looking at here on the right is the details of the policy. This was for just a $250,000 benefit for me, but what is important to notice here is that there are 2 columns that detail what my premium will be over time.

There is a guaranteed amount, meaning that they guarantee the premium will not rise above this amount over time. So, it begins at $179 per year, but as you can see, can drastically increase over time to become more than 5 times higher 14 years from now!

This increase will depend on a lot of factors over the next 20 years, the company’s profitability, performance of investments, inflation, and so on. What’s just important to realize is that there is huge uncertainty in what your premium will be in the future.

And then there is a non-guaranteed column, an optimistic scenario for what your premiums will be over time. This is the rosy scenario that they will focus on.

In the chart above I graphed out the annual premiums over time for these 2 options. The guaranteed in blue and the optimistic scenario in yellow. And then I also put in green the cost I was quoted for a level term policy, which was $220 per year.

And you can see that initially these annual renewable policies can be cheaper, but they always become more expensive over time. Either one of the blue or yellow scenarios ends up costing you more over time.

So if you have one of these types of policies instead of a level term policy. You should ask yourself if this type of policy is appropriate. Is it worth saving a little money early on for a potentially much larger cost in the long run?

And also, if you are in one of these policies before the premium has started its dramatic increase, should you look at finding a replacement policy that provides more certainty in your premiums and benefits?

Want help determining the right type, and amount, of insurance for you? That is just one part of our financial planning services! Click Here to schedule a free 30-minute meeting with us to see how we have helped households just like yours with their financial and retirement plan.

Permanent Life Insurance (Whole, Universal)

Now, onto permanent life insurance. This is any variation of whole life, or universal life insurance.

They are called permanent life because as long as you continue to pay the premium, or as long as you pay a minimum amount into the policy, you will always have a life insurance benefit.

These are marketed very heavily. Agents are highly incentivized to sell these types of policies, and they are often pitched as a way to combine saving and insurance all in one product. But first and foremost, realize that they are life insurance first, and savings second.. and a very distant second at that. If you don’t have a need for insurance, the fact that you can save into these is not going to make them useful or worthwhile.

And so right away I hope the idea of permanent insurance highlights a big difference from our chart on the first slide showing insurance need declining over time.

Permanent policies tend to do the exact opposite, lower insurance amounts early on, and increased amounts later on.

For example, on the right side of the image above is the whole life policy I was pitched when I went into Northwestern Mutual. Remember for a 20-year level term I was quoted $220 per year for $250,000 in benefits.

Now with whole life, I was quoted a premium of $3,250 for benefits that would start at just $234,000.

And then, over time as long as I continue to pay a little over $3,000 per year, my insurance benefit will increase. By the time I’m 65 they project it may be $489,000 in benefits. Of course, this asterisk up here points to some print saying this is far from guaranteed and will depend on a host of different factors.

But regardless, this policy is going to function quite differently than the term policy we looked at previously. I get less insurance early on, when I actually need insurance by the way, and now I have a lot more later on, when as long as I continue saving according to my plan, I won’t need.

Oh, and it costs $60,000 more over the course of my life for this insurance as well compared to the term policy.

This is a whole life example, then there is also universal life which tends to have lower premiums, but much more variability in benefits and premiums over time.

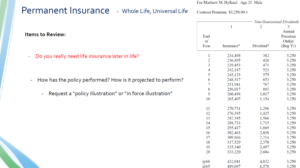

Because of that, if you have a universal policy that you have not reviewed in a while, a good first step is to request an updated policy illustration or sometimes called an in force illustration of the policy to see how it is performing, and how it is projected to perform in the future.

Universal Life Policy Illustration

And that illustration is going to be many pages, but in the back is going to be a few tables that look like this:

A lot of numbers here, but all this is showing you is the premiums you pay over time, in this case it is $9,100 per year, any projected cash value that will build up, and the death benefit over time.

These policies can be structed a lot of different ways, but this is just one example of a joint universal life policy that a client was given. They had the desire to make sure there was a $500,000 benefit for their children to cover some liabilities of their business that the kids would inherit. So this policy only pays out once both spouses have passed.

This household was also very good savers and their business was doing well. They were maxing out an individual 401(k), so building up assets pretty quickly. With enough savings, that build up in savings was eventually going to more than cover their anticipated need.

So, they went to an insurance company and received this quote. Over the course of 20 years they were going to pay $182,000 in premiums, for $500,000 payout only once both spouses had passed away.

And so, a few things jumped out to us right away. First, their need for insurance was really for early on in the plan. As I mentioned, they were good savers adding $25,000 or more per year to their retirement account. Where they needed insurance was in the instance that both of them passed in the first 20 years.

So, we got a term insurance quote as well – and it was a total of $3,000 per year for the premiums instead of the $9,000 here. So, they could receive the same death benefit for the first 20 years, and save $6,000 per year or potentially about $120,000 in premiums….pretty significant!

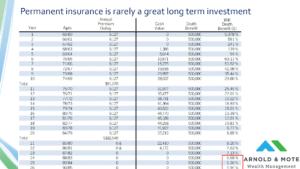

Universal Life Insurance is NOT a Good Long Term Investment

Then also notice the far right column, which shows the IRR, or the return of the premiums received based on the death benefit. Just for example in year 20 if both parents passed away, they paid in $182,540 and would receive $500,000. This is equivalent to if they invested the premiums and received an annual return of 8.85%.

But, what’s worth noticing is how that return drops over time. Remember the supposed appeal of these policies is the permanent benefit. But, that benefit becomes worth less and less over time.

So, these policies end up being way more expensive than term policies early on, and then end up producing returns that are really just equivalent to a bond return in the long run, but have locked up more than $180,000 over their retirement.

There can be a use for these policies, but this scenario just doesn’t make sense for a lot of scenarios we encounter.

Options for Unnecessary Permanent Insurance Policies

So if you have one of these permanent policies and determine that it is no longer needed or appropriate for your situation, you have a few options.

You can just surrender the policy. Even if there is no cash value built up, at least this saves you the premiums, which as we’ve seen can be pretty significant.

If this applies to you – See our post here: “Should I Cash Out My Life Insurance Policy?”

If there is cash value, that can create some tax liability. But, there may be some tax planning we can do around this, too!

If you are retiring, you may have very low income, so cashing these out might result in very little in taxes compared to if you did it right now as you are working and have relatively high income, for example. So we can build this into your withdrawal plan in retirement and get it out in a tax efficient way, and put that money to much better use than permanent life insurance.

Then, there is also a way to exchange these policies tax free as well. This might be useful if you have a very large cash value and can find a different policy that has features that are more approrpate for you. For example, maybe a policy that also has long term care insurance benefits, or one that provides a more appropriate benefit amount, or gives you better access to withdrawal the cash value of the policy.

Long Term Care Insurance Review

Now, moving on to long term care insurance.

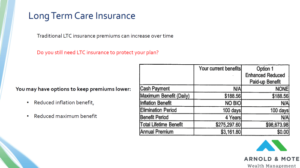

Traditional long term care policies are pretty straightforward. You pay a premium, though that premium is rarely fixed like level term insurance. And receive a set benefit.

As any of you who have this type of insurance know, it is expensive. So just like with life insurance, the big question to ask yourself is do you still need this insurance?

It may have been very smart to buy this when you were 60 years old and at risk for an early long term care scenario. But if you are 75 now and have been healthy and your savings have done well, you may be in position to not need this insurance any more and be much more confident in self-insuring.

Like life insurance, the need for this type of insurance can decline over time.

These types of policies, and particularly if you purchased a long term care policy many years ago, have seen big increases in their premiums. They were just not priced correctly and a lot of insurance companies lost a lot of money on these.

So, another scenario you will probably be presented with if you have one of these policies is an offer to reduce the benefits in exchange for a reduction in your require premium.

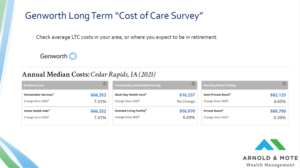

Costs of Long Term Care

In order to determine if that long term care insurance policy is still needed, one big variable to consider in your plan is what a potential long term care stay will cost you.

Thankfully, there’s a good resource to help you with this

The insurance company Genworth does a big annual survey of long term care costs across the country and publishes their results on their long term care calculator, here.

You can type in your zip code, and get up to date information on the costs of various levels of care in your area.

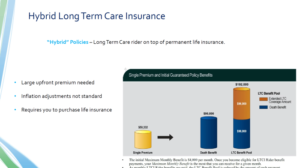

Hybrid Long Term Care Insurance

One final type of insurance we will look at is commonly called hybrid long term care insurance. This is some sort of permanent life insurance combined with long term care insurance.

Like the permanent life insurance mentioned above, from our experience this is heavily marketed. So if you reach out for a long term care insurance quote, be ready to look at a policy like this.

These are touted as a way to get life insurance, but insure that a portion of the death benefit would be available to help cover long term care insurance costs.

in general, we find that these policies just don’t make sense for most of our clients. Why?

First, they usually require large upfront payments of premium. Below we are looking at a quote a client received for a policy that had $96,000 in life insurance benefits, and $96,000 in additional benefits that could be used for long term care expenses.

This client was in their mid 50s, and had done a great job of saving for retirement. They had $2 million in retirement accounts, would have strong fixed income in retirement from pensions and social security, and were performing Roth conversions to reduce tax liability later in their plan.

For this policy, the insurance company required an up front one-time payment of $50,000!

It was very likely that this client would not need this coverage for 2 or more decades. By them giving up $50,000 today or a maximum benefit of $96,000 at some date well in the future is not a good return! They would more than likely just be better investing that $50,000 in a brokerage account.

Also, this required this family to purchase additional life insurance that they didn’t need. Remember, they had more assets than they needed for their plan. $96,000 in life insurance was just not needed.

Lastly, one big downside to hybrid life insurance is that the long term care benefit is usually not inflation adjusted. 20+ years from now, $96,000 may not even pay for a single year of a nursing home!

Traditional long term care policies can be purchased with inflation protection, and do not require the purchase of additional life insurance. For that reason, we find basic long term care insurance to be the better fit for most of our clients and tend to recommend avoiding these hybrid policies.

Get Help With Your Insurance Review

Insurance is complicated – So get help! We offer free 30-minute meetings to hear how we work with clients and help answer your questions regarding insurance, or any other part of your financial plan! Set up your free, no obligation meeting with us here.

Matt Hylland is a financial planner and partner at Arnold & Mote Wealth Management, where he helps individuals and families make informed decisions around retirement planning, investment management, tax planning, and comprehensive financial strategy. As a flat-fee, fiduciary advisor, Matt focuses on providing objective guidance designed around each client’s goals and long-term financial needs.

Before transitioning into financial planning, Matt worked as a materials scientist for the Department of Defense, bringing a problem-solving mindset and analytical approach to his work with clients. He has been featured or quoted in nationally recognized financial publications, including The Wall Street Journal, CNBC, and Kiplinger, for his insights on personal finance and investing.

Years of experience: 10

Specializations: retirement decisions, tax-efficient strategies, investment choices, and the complex financial decisions that come with major life transitions.