Covered call funds offer investors the prospect of much higher dividend payments than regular index funds. Funds that follow a covered call strategy have attracted tens of billions of dollars over the last few years. We believe there are feature of these funds that have significant drawbacks for most investors that make them a poor investment.

This next type of investment we are looking at is what are generally named covered call funds, but sometimes have creative marketing departments that might use the term enhanced income, equity income, or some variation of that.

JEPI – Covered Call ETF Example

Why is this topic on the list? I have a screenshot here of an ETF managed by JP Morgan, the fund is the JP Morgan Equity Premium Income ETF, ticker symbol JEPI.

This was one of the hottest new funds in the last few years, this fund alone went from $0 to over $30 billion in assets in the last 3 years since its launch.

What jumps out to you? The 7% dividend yield is nice, paid as a monthly dividend, and I think that’s a huge reason these funds get a lot of attention.

Then you can see some of the marketing speak here down below. Monthly income, stock market exposure but with less volatility. What’s not to love about that?

How Do Covered Calls Work

The fund management pretty simple – they own stocks, and then sell call options on the stocks that they hold.

What exactly does selling a call option mean?

Call Option Basics

Options and other derivatives can get complicated really fast, but at a very simple level, a call option is just a right to purchase a stock at a certain price, this is known as the “Strike Price”, within a certain time period.

For example. Here are the details of Apple’s stock yesterday when the market closed, it was about $188 per share. And below that I am showing details of call options that exist for Apple shares.

And what this option data shows you is that I can purchase a call on Apple that gives me the right to purchase a share of Apple for $190 per share for $.41.

In other words, if I buy this option for 41 cents, I can buy a share of apple for $190 no matter the price. If Apple jumps up to $200 per share tomorrow, if I have this option I can buy that share for $190.

If apple never reaches $190, my option expires worthless and I lose my 41 cents.

Selling a Call Option

So buying options is relatively straightforward. But these funds are not buying call options, they are selling them.

In this case, the fund owns Apple shares and is selling the $190 option. If Apple shares never rise to $190, the fund is pocketing the 41 cents and going on its merry way.

But if Apple rises above $190, the fund still keeps the 41 cents, but is now also selling its Apple share for $190.

Pros and Cons of Covered Calls

Hopefully that quick example made sense, but if not, don’t worry you don’t have to understand the details to understand the pros and the cons to investing in this type of fund.

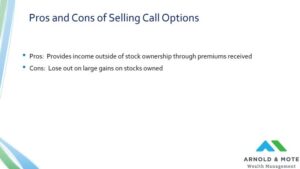

For the primary advantage for these types of funds, it can provide extra income than what you receive from general stock ownership. If your calls are never exercised, you keep the 41 cent option premium, keep your stock, and just got a little extra income than you would have received otherwise.

The downside, and this is very significant over the long run as we’ll see in a minute – is that you have a risk that you lose out on most of the gains in the stock market. And that is because when you sell an option, you essentially set a cap on the gains you can get with that investment. If shares rise above the strike price, you are forced to sell and no longer get any benefit of a rising share price.

JEPI ETF Performance

I think a few charts will be the best way to show this.

Here is a table of the annual returns for the previous 3 years for JEPI.

Notice 2022 – The S&P 500 was down about 18.1%, not a good year. This fund was only down about 3.5% – that was great and is an example of a time when these types of funds do better. They do better because in a falling market, the shares are not getting called away, so the fund is just collecting that options premiums, the 41 cents in our previous example, as an extra bonus.

So 2022 happened, and billions of dollars flowed into this fund. What happened the next year?

2023 was a big year for the stock market, the S&P 500 was up about 26.3%. Meanwhile JEPI was up only about 9.9%. Why did this happen? When the stock market rose, the shares that JEPI had got called away and the fund only participated in a portion of the rise in the market.

2023 is a perfect example of the risk in these types of funds

JEPI vs SPY

How has the JEPI ETF performed against the general stock market?

As you can see, despite outperforming the market significantly in 2022, the fund has produced very low returns in 2021 and 2023 that has led to it underperforming the general stock market significantly.

QYLD vs QQQ

Another example of a fund that sells covered calls is an ETF with the ticker symbol QYLD. This fund sells call options on stocks within the NASDAQ-100 index. This fund is smaller, with less in assets under management than JEPI, but it has a much longer history. This allows investors to see the real cost of a covered call strategy over the long term.

Here you can see, despite QYLD outperforming QQQ over several years, the cap that a covered call strategy puts on your annual returns when the stock market rises is too significant to make the tradeoff worthwhile.

Summary of Covered Call Funds Pros and Cons

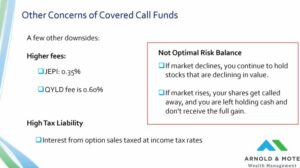

These funds have a few other downsides as well.

First, they have much higher costs than a regular index fund. JEPI has a relatively low fee for this type of fund, only about 35 basis points. QYLD is higher with a fee of 60 basis points. Many fund that sell covered calls for income have fees near 1%.

Over time, this high fee eats away at investor returns and further impacts investors realized performance.

Second, these funds are very tax inefficient. Much of the income these funds produce is taxed at income tax rates, and the frequent trading within the funds can lead to additional short term capital gains tax distributions.

If you are set on using these types of funds that sell covered calls, utilize a Roth IRA, 401(k), or IRA instead of a brokerage account if able.

And ultimately, if you just think about the risk balance these funds offer investors, you should be able to see why they are not favorable for long term investments.

Investors in covered call funds still hold stocks as the market declines. Yes you receive some additional dividend income, but if Apple drops 40%, the fund is still holding Apple shares that are declining. Investors still have significant exposure to the stock market declining.

Then, if the market rises, your shares get called away and you do not appreciate in the gains. Remember in 2023, the S&P 500 returned about 26% and JEPI returned under 10%. In order to receive attractive long term returns, you must be in the market when years like 2023 come around. Capping your returns makes it impossible to achieve long term compounding returns that the stock market has provided to other investors.

Matt Hylland is a financial planner and partner at Arnold & Mote Wealth Management, where he helps individuals and families make informed decisions around retirement planning, investment management, tax planning, and comprehensive financial strategy. As a flat-fee, fiduciary advisor, Matt focuses on providing objective guidance designed around each client’s goals and long-term financial needs.

Before transitioning into financial planning, Matt worked as a materials scientist for the Department of Defense, bringing a problem-solving mindset and analytical approach to his work with clients. He has been featured or quoted in nationally recognized financial publications, including The Wall Street Journal, CNBC, and Kiplinger, for his insights on personal finance and investing.

Years of experience: 10

Specializations: retirement decisions, tax-efficient strategies, investment choices, and the complex financial decisions that come with major life transitions.