Inflation is a retirees worst enemy. Here’s how to allocate your investments to protect yourself from inflation:

Investing with Inflation

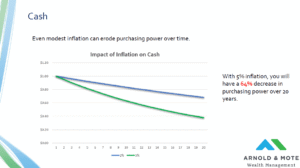

While it rarely makes big impacts in any single year, over time even modest inflation results in significant reduction in purchasing power of your savings.

Even with just 3% inflation, the value of a dollar will be reduced by more than half over a 30 year period.

Inflation is particularly damaging to retirees because they are the ones usually more reliant on fixed income, such as pensions, Social Security, and savings instruments like CDs, bonds, and savings accounts. These assets produce an income stream that has little or no inflation adjustments, meaning that their real value to you declines significantly over time.

There are a few things you can do to make sure your retirement portfolio is positioned as well as it can be for handling rising inflation.

Diversify (Don’t put all your eggs in one basket)

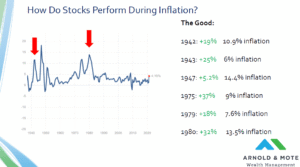

Many retirees thought gold would be a good inflation hedge in the early 1980s. However, the metal’s price declines more than 80% adjusted for inflation over the next 20 years.

What worked better than gold? A diversified basket of stocks had a much higher return and was much less volatile.

Want to know more about investing in Gold – Watch our webinar

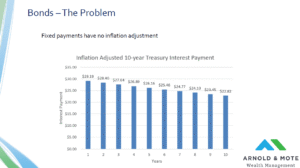

Reduce Duration of Bonds

Long term bonds, where your money is locked up for 10 years or more, will see much more negative impact from inflation than shorter term bonds. A portfolio of shorter term bonds will also let you invest at higher interest rates more quickly than if you had longer term bonds.

Inflation is certainly not a risk to ignore. As fiduciary financial advisors, we can help you create a financial plan and stress test that plan through various scenarios, like rising inflation.

Looking for more on inflation? Here’s a webinar we did for clients with much more detail on how to invest with inflation in mind

Matt Hylland is a financial planner and partner at Arnold & Mote Wealth Management, where he helps individuals and families make informed decisions around retirement planning, investment management, tax planning, and comprehensive financial strategy. As a flat-fee, fiduciary advisor, Matt focuses on providing objective guidance designed around each client’s goals and long-term financial needs.

Before transitioning into financial planning, Matt worked as a materials scientist for the Department of Defense, bringing a problem-solving mindset and analytical approach to his work with clients. He has been featured or quoted in nationally recognized financial publications, including The Wall Street Journal, CNBC, and Kiplinger, for his insights on personal finance and investing.

Years of experience: 10

Specializations: retirement decisions, tax-efficient strategies, investment choices, and the complex financial decisions that come with major life transitions.