The Net Investment Income Tax is an added tax that is charged on dividends, interest, and capital gains from your investments. It can also apply to many other forms of income, such as rental property income, passive business income, and even certain annuity payments.

When Does the Net Investment Income Tax Apply?

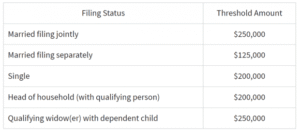

The tax applies only to individuals and trusts with a MAGI, or Modified Adjusted Gross income, over a certain threshold. This income limit threshold is set by the Internal Revenue Service and changes based on your tax filing status (Married filing jointly, married filing separate, or single filing), but will begin to trigger for most households at either $200,000 or $250,000 in MAGI.

How Much is The Net Investment Income Tax?

If your income is high enough to cause you to be subject to the tax, you will face an extra 3.8% tax on your investment earnings or a 3.8% tax on the amount that your annual income in excess of the income threshold noted above.

What Counts as Investment Income for the NIIT?

Here are a few examples of types of income that count towards the net investment income tax (these are common items, but the list is not all-inclusive):

– interest (from bonds, bond ETFs or mutual funds, bank CDs, money market funds, series I savings bonds, etc)

– dividends (from stocks, stock etfs and mutual funds, REIT dividends, etc)

– capital gains (long-term and short-term)

– rental income

– royalty income

– withdrawals or payments from non-qualified annuities

– income from businesses that are passive activities to the taxpayer (“Passive income”)

What Does Not Count as Income Subject to the NIIT?

Here are examples of income that does not count towards the net investment income tax (these are the most common items, but is not all-inclusive):

– Wages

– unemployment compensation

– operating income from a nonpassive business

– Social Security Benefits

– alimony

– tax-exempt interest (such as from municipal bonds)

– self-employment income

– distributions from certain qualified retirement plans such as 401(k)s, 403(b)s, and traditional IRAs

Example of NIIT Liability

For someone who relies on dividends and interest to fund their retirement, or those who use their investments for large purchases such as a house or car in retirement, this tax can easily amount to many thousands of dollars.

Consider a couple who file their taxes jointly and are near retirement, but currently with high income. They have a combined $200,000 in W-2 wage income, and receive $20,000 in dividends and interest from their investments.

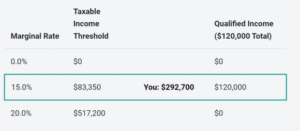

They want to purchase a retirement home now, which requires a $150,000 down payment that they plan to take from their taxable brokerage account. Assume the $150,000 in investments they sell have a cost basis of $50,000, so $100,000 in gains are taxed at long term capital gains rates on their tax return.

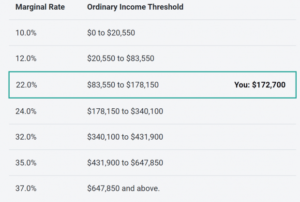

This couple has an MAGI of $320,000, and taxable income of $292,700.

They would find themselves in the 22% Federal income tax bracket:

And their capital gains tax bracket is 15%:

But in addition to these regular income taxes and capital gains taxes, they would also pay an additional $2,660 in taxes due to the Net Investment Income Tax, which would be calculated and reported on their tax returns on IRS form 8960.

For this example, their NIIT liability is calculated by taking 3.8% of $70,000. ($70,000 is the amount their MAGI is in excess of the income threshold noted in the table above).

How to Avoid The Net Investment Income Tax

What can you do to avoid this tax?

A little bit of planning can go a long way. If you can split large investment sales over two tax years, you could dramatically reduce the amount of income or capital gains subject to the tax.

Proper investment account maintenance can also help prevent the net investment income tax as well. Things like tax loss harvesting, or purposely recognizing small gains to raise your cost basis over time can help reduce the impact of this tax later on.

If you are retired and find yourself frequently hit by the net investment income tax, consider QCDs (Qualified charitable contributions) or creating a Roth Conversion plan to reduce future required withdrawals and income.

Creating a Financial Plan for You

If you are trying to do this yourself, you’ve likely found that tax planning, particularly planning around creating tax-efficient retirement plans is complex.

We help our clients create financial plans that help you meet your goals and reduce your tax liability. We offer free 30-minute consultations here so that you can find out if we are the right fit for you and your retirement plan.

Matt Hylland is a financial planner and partner at Arnold & Mote Wealth Management, where he helps individuals and families make informed decisions around retirement planning, investment management, tax planning, and comprehensive financial strategy. As a flat-fee, fiduciary advisor, Matt focuses on providing objective guidance designed around each client’s goals and long-term financial needs.

Before transitioning into financial planning, Matt worked as a materials scientist for the Department of Defense, bringing a problem-solving mindset and analytical approach to his work with clients. He has been featured or quoted in nationally recognized financial publications, including The Wall Street Journal, CNBC, and Kiplinger, for his insights on personal finance and investing.

Years of experience: 10

Specializations: retirement decisions, tax-efficient strategies, investment choices, and the complex financial decisions that come with major life transitions.