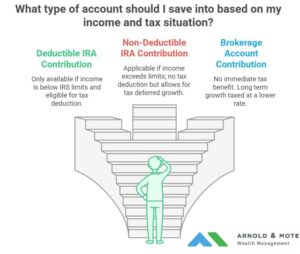

Non-deductible IRA contributions are a common option for savers to get more money into retirement accounts. While saving into an IRA is certainly never a bad idea, we find that for most high income households or households with a high savings rate, basic brokerage account contributions are more tax efficient, and better option for long-term retirement savings than non-deductible IRA contributions.

What is a Non Deductible IRA Contribution?

For many, contributions to a traditional IRA can be tax deductible or essentially made with pre-tax dollars. However, if you are covered by a workplace retirement plan (a 401(k), 403(b), or other employer-sponsored retirement plans) you are not allowed to make pre-tax contributions to IRAs if your household modified adjusted gross income is above the IRS income limits (which for 2025 is $143,000, however there are exceptions for non-covered spouses).

Further, households in this category are also usually unable to make Roth IRA contributions as well since their income is above the maximum income limitations set by the IRS to be eligible for Roth IRA contributions.

However anyone, regardless of income, is able to make a contribution to a traditional IRA up to the annual contribution limit, but receive no tax deduction for the contribution. This is commonly referred to as a Non-Deductible IRA Contribution.

How Are Non Deductible IRAs Taxed?

To determine if an IRA or brokerage account is better for you, you must first understand the tax rules around these two accounts.

With a nondeductible contribution, you don’t receive a tax deduction at the time of contributing. However, the money in the account will grow tax deferred. This is commonly cited as a benefit of doing a non-deductible IRA contribution.

While this may be valuable for a select few, we find that many of our clients see no long-term tax benefit to saving in a non-deductible IRA. In fact it may end up costing them much more in taxes in the long run

This is because any gains you see from the investments in a non-deductible IRA will be taxed at ordinary income tax rates when you withdrawal the money in retirement. Compare this to a standard brokerage account where gains are taxed at long term capital gains rates.

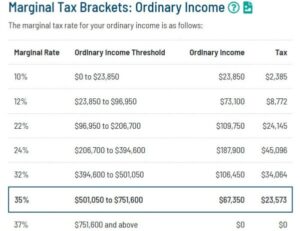

Federal income tax rates are much higher than the long term capital gains tax rates. Your exact tax rates will depend on your other sources of income. But for example, here are the ordinary income rates that the gains on a non-deductible IRA would be subject to in 2025 for household with a married filing status:

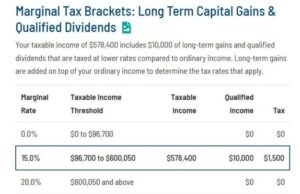

And for comparison, here are the tax rates for long term capital gains, which a brokerage account would be subject to:

Notice that at any income level, the tax rate on capital gains are lower. But there are a number of “sweet spots” that make long term capital gains a much better option to reduce taxes. First, below about $96,700 in taxable income long term capital gains are taxed at 0%. This is a huge opportunity for a lot of retirees!

For high income households the 15% tax rate of long term capital gains are significantly lower than income tax rates. For example, a household with $207,000 in taxable income would have gains from a non-deductible IRA taxed at 24%. Whereas gains in a brokerage account are taxed at just 15%.

Advantages of Brokerage Account Vs IRAs

Besides the potentially lower tax burden, taxable brokerage accounts also have many more tax advantages:

They allow you to tax loss harvest. This can provide a tax deduction of up to $3,000 for you when the stock market declines. While this requires a little more management over time, the tax break can be very valuable for high income households. And, this provides a tax deduction that is not available at all if you contributed to an IRA!

Also, brokerage accounts are much more flexible. You can access the money at any time, and better control your taxes from withdrawals. This is valuable for anyone, but especially valuable for early retirees, or retirees that plan on having years with high expenses. For example, buying a retirement home, cars in retirement, or big vacations.

Taxable accounts also have no contribution limits. While traditional IRAs have limits to the amount you can contribute each year (for 2025 that is either $7,000 or $8,000 depending on your age), brokerage accounts have no limit. You can contribute hundreds of thousands of dollars to brokerage accounts if you want to.

Brokerage accounts do not have required minimum distributions, like traditional individual retirement accounts. For those who save aggressively, very large IRA balances can create huge tax bills later in retirement because of the increasing minimum distributions as you age. We cover this topic in much more detail in our comprehensive guide on Roth conversions.

Lastly, taxable investment accounts have little to no administrative burden when it comes to filing your taxes. Doing non-deductible contributions can be a tax and recording keeping burden. This becomes especially burdensome to track if you have both deductible and nondeductible contributions over time. Each year you will have to file a tax form 8606 to keep track of the after-tax basis for the IRS. Withdrawals in retirement add more complexity as well.

Advantages of Non-Deductible IRAs

There is one big advantage to doing nondeductible IRA contributions, however. And that is the protection from creditors that IRAs provide. If you are ever involved in a bankruptcy or lawsuit, money that you have saved in IRAs is generally protected, though be sure to check with the laws of your state to verify. We would typically recommend reviewing your umbrella insurance if this is a concern.

The tax deferral of non-deductible IRAs can be an advantage for some. If you are in a very high tax bracket, taxes on dividends, particularly non-qualified dividends, and capital gains can lead to a drag on your performance. However, we find that this is quite rare.

If you are very sensitive to capital gains associated with dividends and interest from investments in a taxable brokerage account though, this could be a consideration. For those in some of the highest marginal tax brackets, a proper investment strategy using tax-efficient mutual funds and ETFs will be very important.

Backdoor Roth Contributions – When Non-Deductible Contributions Make the Most Sense

The one exception that makes non-deductible IRA contributions better for just about anyone is if you are eligible to do a “Backdoor Roth contribution.

This strategy involves making a non-deductible contribution to an IRA, and then immediately converting that traditional IRA to a Roth IRA.

This strategy can have much better long term tax advantages because your funds are able to grow and compound tax-free with the Roth account rather than in a taxable brokerage account. However, this options is generally only advisable for those that have no other funds in their traditional IRA, or at least a very low balance. If you have a large IRA balance, from a prior 401(k) rollover for example, than this strategy may not have any benefit to you.

We won’t get into all of the details of this strategy here, but see our Backdoor Roth Contributions blog post for more information on this strategy.

Get Tax Planning Help From a Financial Advisor!

If you are in a position where you are considering doing nondeductible contributions, please reach out. A plan from a financial and tax advisor can prevent significant tax troubles in your retirement. Creating tax-efficient savings and retirement distribution plans is just one of the many financial planning services we offer to our clients.

Matt Hylland is a financial planner and partner at Arnold & Mote Wealth Management, where he helps individuals and families make informed decisions around retirement planning, investment management, tax planning, and comprehensive financial strategy. As a flat-fee, fiduciary advisor, Matt focuses on providing objective guidance designed around each client’s goals and long-term financial needs.

Before transitioning into financial planning, Matt worked as a materials scientist for the Department of Defense, bringing a problem-solving mindset and analytical approach to his work with clients. He has been featured or quoted in nationally recognized financial publications, including The Wall Street Journal, CNBC, and Kiplinger, for his insights on personal finance and investing.

Years of experience: 10

Specializations: retirement decisions, tax-efficient strategies, investment choices, and the complex financial decisions that come with major life transitions.