Just once in your lifetime you are allowed to roll money from your IRA to your HSA, or health savings account. This IRA to HSA rollover is called a “qualified HSA funding distribution”.

This move can help you reduce your tax liability and let you tap retirement funds early. But there’s a few things you should know before you make the transfer:

IRA to HSA Rollover – What to Know

First, you must be currently eligible to contribute to an HSA to make the rollover from your IRA.

If you are not currently covered by a high deductible health plan, you can not do a rollover to your HSA from your IRA. In addition to being eligible right now to contribute to an HSA, you must remain in an HSA eligible health insurance plan for at least 12 months after making the HSA funding distribution.

If you switch part way through this 12 month testing period, you will be subject to additional taxes and penalties.

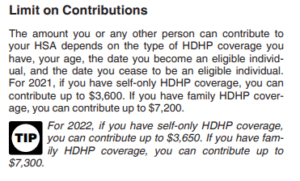

Fund Your HSA From Your IRA – Limits

The rollover amount you are able to do is capped at the annual contribution limit for your HSA.

This amount varies depending on if you are on an individual or family plan and increases each year with inflation. IRS publication 969 will have the up to date numbers.

And, this rollover amount counts as your contribution. You can not contribute the max amount to your health savings account and then also rollover an additional amount in the same year.

Advantages to an HSA Rollover – Tax Benefits

Why should you utilize this opportunity to move money from an IRA to an HSA?

First of all, it will reduce your tax liability. Whenever you go to withdrawal money from an IRA it will be taxed like income. An HSA on the other hand is not taxed if used for qualified medical expenses.

And one thing we know is that medical care in retirement is expensive. You won’t have a problem finding a qualified expense.

HSAs are also not subject to RMDs, or required minimum distributions like IRAs are. This means that if you don’t have expenses, you can let the assets remain in the HSA and continue to grow and compound tax free.

Access Retirement Funds Early

This rollover also allows you to access retirement funds before age 59 and a half.

If you withdrawal from an IRA before age 59.5, you will be subject to not only taxes but also a penalty. If you have qualified expenses, you can withdrawal money from an HSA at any time.

So, this rollover can be especially beneficial to early retirees or those with large medical bills before age 59.5.

Should You Roll Your IRA into Your HSA?

In general we see HSAs as one of the most valuable types of accounts to have in retirement after age 65, and taking advantage of this once in a lifetime opportunity to transfer assets from an IRA to an HSA is something that most who are able to, should take advantage of.

Matt Hylland is a financial planner and partner at Arnold & Mote Wealth Management, where he helps individuals and families make informed decisions around retirement planning, investment management, tax planning, and comprehensive financial strategy. As a flat-fee, fiduciary advisor, Matt focuses on providing objective guidance designed around each client’s goals and long-term financial needs.

Before transitioning into financial planning, Matt worked as a materials scientist for the Department of Defense, bringing a problem-solving mindset and analytical approach to his work with clients. He has been featured or quoted in nationally recognized financial publications, including The Wall Street Journal, CNBC, and Kiplinger, for his insights on personal finance and investing.

Years of experience: 10

Specializations: retirement decisions, tax-efficient strategies, investment choices, and the complex financial decisions that come with major life transitions.