Let's Get Started

You'll get the most value from financial planning if your specific goals and needs match a firm's philosophy and services. Let's learn more about each other.

Ready to Get Started?

You should consider withdrawing from your annuity early in retirement (before starting Social Security) – Withdrawals are taxable, but your overall income may be lower at this stage, letting you take money out at lower tax rates while also helping you delay Social Security for a bigger future benefit.

Annuitizing your annuity provides guaranteed lifetime income but locks up your savings and limits flexibility.

Withdrawing from an annuity instead of annuitizing can reduce fees, offer flexibility, and take advantage of lower tax rates early in retirement.

If you have been saving in an annuity and are nearing retirement, you have a decision to make about how to withdraw money from your annuity in retirement. Depending on the type of annuity you have you’ll have many options, with different tax implications, on how to get money out of your annuity as a retirement income option. Here’s a few items to consider:

Annuities are used to help savers defer interest on their savings while they are still accumulating assets, and then designed to eventually begin paying a fixed monthly payment for your lifetime. If you don’t want to lock up your savings and have a fixed payment for the rest of your life, you may have other options to get money out of an annuity.

The first thing you should ask yourself is how much fixed income you need in retirement. This is any regular fixed amount you receive, like Social Security, a pension, or payments from an annuity. We can help you answer that question, or you may just desire a certain amount of fixed income to cover basic living expenses.

If you need additional fixed income to feel comfortable in retirement, an annuity can be a good way to get that. You can simply annuitize your annuity or exchange your current annuity into one that offers better payments.

Annuitizing means you lose access to the money you have saved, in exchange for regular monthly payments going forward.

This can be a great option if you are risk adverse and want to set some portion of your retirement savings aside in something safer. You will likely accept lower returns going forward, but as long as you are comfortable this can be a great option to create a level of secure income in retirement.

However, that’s not the best solution for everyone. You may want to consider other ways to get money out of an annuity besides annuitizing.

This can help you save you on fees and taxes, and give you more flexibility in retirement to spend your money as needed.

Most annuities will allow a certain percentage of the account to be withdrawn each year. However, you need to be sure you have the details of your annuity to know the rules that are specific to your contract.

Creating a plan to get money out of an annuity can be beneficial in the long run if you don’t have the need or desire for more fixed income.

There are many scenarios when this strategy can make sense. Here’s a few common situation where it may make sense to withdraw from an annuity:

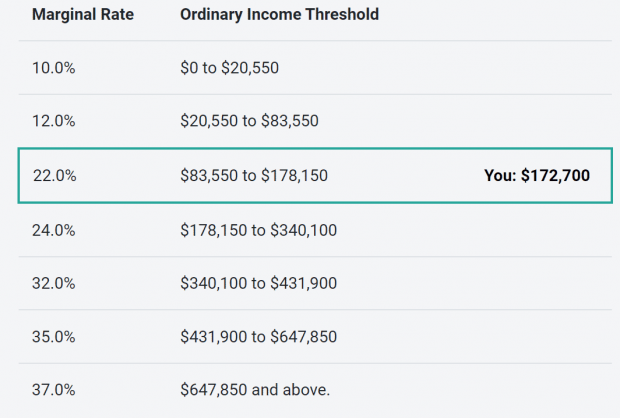

This is because annuity withdrawals will be taxed, and at retirement, you likely have low income and therefore low tax rates. Taking advantage of these low tax rates allows you to get money out of the annuity at the lowest tax rates possible. This allows you to fund your living expenses early in retirement, and perhaps also give you the ability to delay your Social Security to guarantee a higher payment.

One big problem with annuities is their high fees and low growth potential compared to other alternatives. Even if you are very young and decades away from retirement, it may be worth developing a strategy to get money out of your annuity in order to save in lower cost investments that offer more flexibility.

There are different types of annuities, qualified or non-qualified that have very different tax consequences for withdrawals, some have added surrender fees, and if you are under age 59.5 there may be tax penalties for early withdrawals.

Before taking any action, be sure you understand the tax implications of withdrawing from your annuity.

Using these options, while navigating around any penalties or fees, can help you better meet your goals and give you a more tax efficient way to pay for your retirement.

Have a question about how your annuity fits (or doesn’t fit!) into your retirement plan? Reach out today to see how we can help create a retirement plan for you:

Matt worked for the Department of Defense as a material scientist before changing careers to follow his interests in personal finance and investing. Matt has been quoted in The Wall Street Journal, CNBC, Kiplinger, and other nationally recognized finance publications as a flat fee advisor for Arnold and Mote Wealth Management. Arnold & Mote Wealth Management is a flat-fee, fiduciary financial planning firm serving individuals and families in Cedar Rapids and surrounding areas. He lives in North Liberty, where you will likely find him, his wife Jessica, and two kids walking their dog on a nice day. In his free time Matt is an avid reader, and is probably planning his next family vacation.