The SECURE Act of 2020 opened the door for more insurance products to be offered within 401(k) plans.

One trend we’ve noticed creeping into our clients’ retirement accounts —including those employed at Collins Aerospace/Raytheon— is the emergence of target date funds that now contain annuities. These new investments, sometimes called “hybrid target date funds,” aim to provide an autopilot savings plan that secures income for you in retirement.

But are these new investments really right for you?

What is a Hybrid Target Date Fund?

Before you invest, it’s essential to understand how these funds work. By selecting one of these hybrid target-date funds, a portion of your investments within your 401(k) will automatically go into an annuity. Then, as you age, a larger portion of your savings will be channeled into the annuity.

Perhaps it’s no surprise, but we believe most savers should think twice before adding these types of investments to their portfolios. Here are a few reasons why:

Higher Expenses

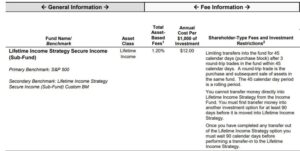

First, any insurance product will typically come with higher expenses. Be sure you understand the fees associated with these investments and how they might impact your account over time.

For example, a local employer near our office, Raytheon (RTX), offers these funds in its 401(k) plan. The fees for someone nearing retirement in one of these funds can exceed 1%.

How Much Income Do You Need?

Second, it’s important to know that these funds are not customized for you. They usually default to having somewhere between 25% and 33% of your money in an annuity by the time you retire.

Is that an appropriate amount for you? They don’t know your financial situation, so it’s highly unlikely that the amount they choose is optimal for you.

Annuitizing your retirement savings is an irreversible decision that should be made carefully. Consult with a financial planner, ideally a fiduciary, fee-only one, to determine how much, if any, annuity income you need in your plan.

Don’t Lock Up Money Now

Finally, know that you’re not necessarily missing out by forgoing these investments now. You can always buy an annuity later, once you roll your 401(k) savings into an IRA. Don’t feel pressured to purchase an annuity now. Instead, get closer to retirement, then decide if you need additional fixed income.

Even if you’re certain an annuity is right for you, you’ll have many more options if you explore those available outside of your 401(k) plan. It’s likely you’ll find a better, lower-cost annuity that suits your needs outside of your 401(k).

Matt worked for the Department of Defense as a material scientist before changing careers to follow his interests in personal finance and investing. Matt has been quoted in The Wall Street Journal, CNBC, Kiplinger, and other nationally recognized finance publications as a flat fee advisor for Arnold and Mote Wealth Management, a flat fee, fiduciary financial planning firm serving individuals and families in Cedar Rapids and surrounding areas. He lives in North Liberty, where you will likely find him, his wife Jessica, and two kids walking their dog on a nice day. In his free time Matt is an avid reader, and is probably planning his next family vacation.